At Atveris, we provide high‑quality emissions verification aligned with the ISO 14064-3 standard. We also support a wider range of sustainability disclosures, especially as independent assurance becomes increasingly expected across global markets. As expectations around climate reporting continue to tighten, organisations must demonstrate that their GHG inventories rely on transparent methodologies, traceable evidence, and credible third‑party review. In many cases, this is no longer optional. Instead, it forms a core component of regulatory compliance and investor confidence.

Where GHG verification is required

California SB 253

Under SB 253, companies must disclose scope 1 and scope 2 emissions first, with scope 3 phased in later. The law requires the use of an independent assurance provider applying recognised verification standards such as ISO 14064-3, ISO 14065, AA1000, or AICPA.

CSRD (Corporate Sustainability Reporting Directive)

Under the CSRD, companies are required to disclose climate and emissions information in line with the European Sustainability Reporting Standards (ESRS), including scope 1, 2, and 3 emissions where material. As a result, companies now prioritise more robust, auditable methodologies and stronger internal governance to meet assurance expectations.

EU Emissions Trading Scheme (ETS) / UK ETS

The EU and UK ETS both require annual monitoring, reporting and verification of emissions. These requirements have existed for many years; however, the level of scrutiny continues to rise as regulators focus more closely on data completeness and calculation accuracy.

CBAM (EU Carbon Border Adjustment Mechanism)

With the transitional phase complete, importers must now submit fully verified embedded emissions in their annual CBAM declarations. The scheme places strong emphasis on traceable, source‑level evidence. Consequently, companies need high‑quality GHG inventories that can withstand rigorous verification and clearly demonstrate the reliability of underlying data.

Where GHG verification is widely used

SECR (UK Streamlined Energy and Carbon Reporting)

SECR does not mandate verification. However, many organisations still obtain third party assurance because it provides a clear evidence trail, strengthens internal governance, and reduces the risk of inconsistencies across global disclosures.

Voluntary GHG inventories (ISO 14064-1 / GHG Protocol)

Although ISO 14064-1 verification is optional, organisations frequently adopt it to validate their methodologies, support internal carbon pricing or prepare for future regulatory requirements. Furthermore, independent review reassures internal and external stakeholders that the inventory uses reliable data.

ISSB / IFRS S2 aligned climate disclosures

ISSB does not mandate verification, but organisations frequently seek independent review of their emissions data because these figures underpin climate related risk analysis. Verification reduces the likelihood of restatements and increases confidence among lenders, investors, and audit committees.

CDP

CDP strongly rewards independently verified GHG inventories, especially for organisations aiming for A or A‑ lists. Verification demonstrates that disclosures rely on consistent methodologies and defensible evidence. As a result, many companies pursue verification to strengthen alignment across their reporting and achieve higher scoring outcomes.

Why GHG verification matters

A GHG inventory sits at the center of climate target setting, risk assessment, regulatory reporting, and investor communication. If the underlying numbers are unreliable, the rest of the reporting structure becomes exposed to challenges. Verification provides:

- Confidence that emissions are calculated consistently with ISO 14064-3 and the GHG Protocol, with transparent methodologies and traceable data

- Clear identification of gaps, errors, or inconsistencies, reducing uncertainty where disclosures inform financial reporting or regulatory filings

- Enhanced credibility with investors, boards, and auditors, who increasingly expect independent verification even when not mandatory

- Improved readiness for future reporting and compliance, supported by clearer documentation, stronger governance, and greater data accuracy

Our verification work often highlights issues that internal teams overlook, particularly in scope 3 categories, emission factor selection, and boundary definitions, helping organisations address problems before they affect regulatory filings or wider disclosures.

What we verify as part of GHG assurance

We currently focus on GHG inventories and emissions data verification. This includes:

- Scope 1, scope 2, and scope 3 inventories prepared under ISO 14064-3 and the GHG Protocol, while closely monitoring the emerging international assurance standard ISSA 5000

- Calculation methodologies, emission factors, and activity data evidence

- Organisational boundaries, including operational control, financial control, and equity share approaches

- Category‑level assessments for material scope 3 sources

- Consolidation and reconciliation checks across business units or regions

Verification engagements may be limited assurance (often used for compliance or first‑time reporting) or reasonable assurance (appropriate for more mature inventories or higher‑scrutiny filings).

Our approach

We follow the principles and structure of ISO 14064-3, applying a risk based methodology that prioritises material emissions sources and areas with higher uncertainty. The verification focuses on evidence, transparency, and consistency.

We assess:

- Completeness and appropriateness of activity data

- Selection and justification of emission factors

- Accuracy of calculations, including independent recalculation

- Documentation of assumptions, exclusions, and methodologies

- Controls and data management processes across the reporting boundary

Our objective is to provide a verification statement that clearly reflects the reliability of the inventory, while also giving practical, actionable recommendations.

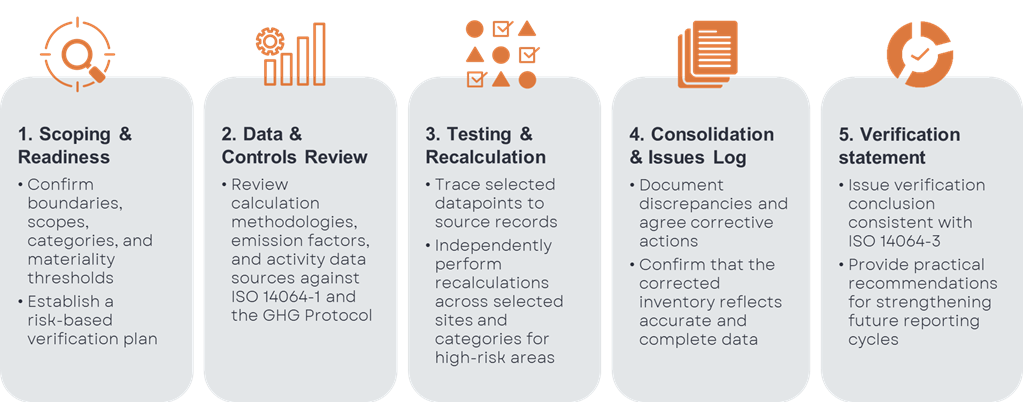

Our GHG verification process

Working with Atveris

At Atveris, we take a focused, technical approach to GHG verification. We have a clear aim to support companies with verification to ensure they have a reliable, defensible emissions inventory that stands up to regulator, auditor, and investor scrutiny. Our engagements are structured to align with your reporting timelines, and our recommendations support continuous improvement across future cycles.

Whether your priority is regulatory compliance or strengthening voluntary GHG reporting, we can support you through the verification process. Contact us at assurance@atveris.com to discuss scope and timelines.